GameStop is bidding for eBay. The market dropped GME 8-10% on the announcement and Polymarket priced the deal at 15% completion odds. Both reactions are correct.

This is a capital deployment story dressed up as strategy. Ryan Cohen has been sitting on a $9 billion cash pile for four years without a coherent operating thesis. The eBay bid is what happens when a CEO with a balance sheet finally has to do something with it.

Here's the math. Here's what's been missed. And here's what $9 billion should have bought instead.

The Numbers

GameStop's peak revenue was roughly $9.6 billion in fiscal 2011. Today the business does about $3.6 billion and shrinking. That's more than 60% of revenue gone.

The peak store count was around 6,600 GameStop-branded core locations. Today the company runs somewhere between 1,600 and 3,200 stores depending on how you count international and ThinkGeek leftovers. They shut 727 U.S. stores in fiscal 2025 alone. That's two stores closing every single day for a year.

Hardware sales fell 31.7% year over year in Q1 fiscal 2025. Software fell 26.7%. The two pillars of the original business are in freefall.

Fiscal 2025 operating income was $232 million. The cash pile is around $9 billion. The T-bill yield on that cash outperformed the entire retail business. Read that sentence again. The Treasury Department made GameStop more money than GameStop did.

And the cash didn't come from earnings. It came from roughly $3.55 billion in 0% convertibles maturing in 2030 and 2032 with conversion prices around $29. Plus ATM equity offerings on top. The war chest is dilution-funded, not earned. Shareholders paid for the cash. And now Cohen wants to spend it.

GME dropped 8-10% the day the eBay bid was announced. The market did the dilution math in real time. Polymarket has the deal at a 15% completion probability.

Pokemon Is the Only Thing Working

Collectibles went from 15.5% of revenue to roughly 33% in two years. That's the bull case Cohen is selling Wall Street.

Strip the Pokemon out and the bull case dies. Pokemon TCG at MSRP is the floor holding the floor up. GameStop is one of the few national retailers actually selling sealed Pokemon product at sticker price during the biggest TCG run in history. People line up. The stores convert. It works.

It works for now.

The problem is concentration risk. If you're a retailer and one IP holder controls a third of your most-hyped category, that IP holder owns you. They can change allocation. They can change partners. They can launch a 30th anniversary marketing program with a different retailer and not tell you.

Spoiler. They did. We'll get there.

The eBay Bid Is a Capital Deployment Story Dressed Up as Strategy

Here's the actual Cohen pitch on eBay.

Cut sales and marketing from $2.4 billion to $1.2 billion. Take out $20 billion in financing from TD Securities. Gut headcount. Run the synergies. Harvest the brand.

That's not a strategy. That's a roll-up. It's the Toys R Us playbook. The Sears playbook. The JCPenney, RadioShack, Bed Bath & Beyond, Payless, Mervyn's, Linens 'n Things, Family Dollar pre-spinoff playbook. Look at the list. None of those companies came out the other side stronger. Most of them came out the other side bankrupt.

PE roll-ups in retail have a track record. The track record is a graveyard.

And eBay doesn't need GameStop's stores. eBay already owns Goldin (acquired 2022). eBay already owns TCGplayer ($295 million in 2022). eBay Ventures sits on the cap table of Whatnot, Tradesy, Trove, and Treet. They've been quietly building the vertical infrastructure of every collectibles category for half a decade.

eBay already runs centralized authentication centers for sneakers, watches, and handbags. If they wanted physical drop-off, they could partner with USPS tomorrow. The Postal Service runs 31,000 retail locations. UPS has 5,000 of its own stores plus 20,000 access points. Staples has 1,000. Any of those is a phone call.

GameStop's pitch is "we're the physical authentication layer eBay needs." eBay has six other ways to get that without buying a dying retailer.

And one more thing. Cohen has not done a public investor call in 18 months. Eighteen months. The bid is replacing the call. That's not a CEO communicating a strategy. That's a CEO buying himself a news cycle so he doesn't have to answer questions about the last four quarters.

What $9 Billion Should Have Bought

If you actually wanted to make GameStop a real collectibles company, here is the seven-point version.

1. Buy Hasbro.

Hasbro's market cap is around $13.5 billion. A 30-40% premium puts the deal at $17-19 billion. Cohen has $9.4 billion in cash and a $20 billion financing letter from TD Securities. All-cash. Zero dilution. He could have closed it.

What you get for that check. Magic: The Gathering, doing $1.72 billion in revenue, growing 59%, 37% of Hasbro's total sales. Wizards of the Coast at $2.2 billion in revenue and a 46% operating margin. Dungeons & Dragons. The entire Universes Beyond pipeline. Avatar. Marvel. Final Fantasy. Spider-Man. TMNT. Hobbit. Star Trek. Lorwyn. Over a million organized play participants worldwide.

Every single GameStop in America becomes the de facto MTG flagship in its market. League nights every Friday. Pre-release events every set. Commander tables in the back. Sealed product allocations that move at retail because you own the IP.

That is the Pokemon hedge. That is how you stop being a hostage to a Japanese IP holder you don't control. You own the second-biggest TCG in the world outright. Cohen had the cash and the financing letter on his desk. He didn't make the call.

2. Buy Whatnot.

Whatnot was valued at $5 billion in January 2025. Today it's $11.5 billion. The company is doing $6 billion in GMV, $1 billion in revenue, 60% market share in live shopping across North America and Europe, and 80 minutes per day per active viewer. That's more than YouTube. More than TikTok.

Twelve months of inaction doubled the price. Cohen could have bought the entire live commerce category for the cost of a stock buyback. Instead he watched it double.

3. Buy TAG Grading.

Computer-vision grading. Walk in, scan, slab, walk out. With 1,600 stores you instantly become the only national footprint for instant grading in America. You kill the 75-day PSA mail-in flow on day one.

That's a moat. That's a structural advantage that nobody else can replicate without 1,600 leases.

4. Buy a convention.

Fanatics figured this out three years ago. Own the events, you own the calendar. Own the calendar, you set the secondary market. The National Sports Collectors Convention is acquirable in the low nine figures. Couch change for a company sitting on $9 billion.

5. Build real vaults.

1,600 stores running bonded, insured vaults. On-site grading. Break tables. League play. Trade nights. Distributed vaults beat eBay's centralized model on speed, on local trust, and on customer experience. You can't out-eBay eBay on a server. You can out-eBay eBay on a Tuesday night in Cleveland.

6. Buy grails.

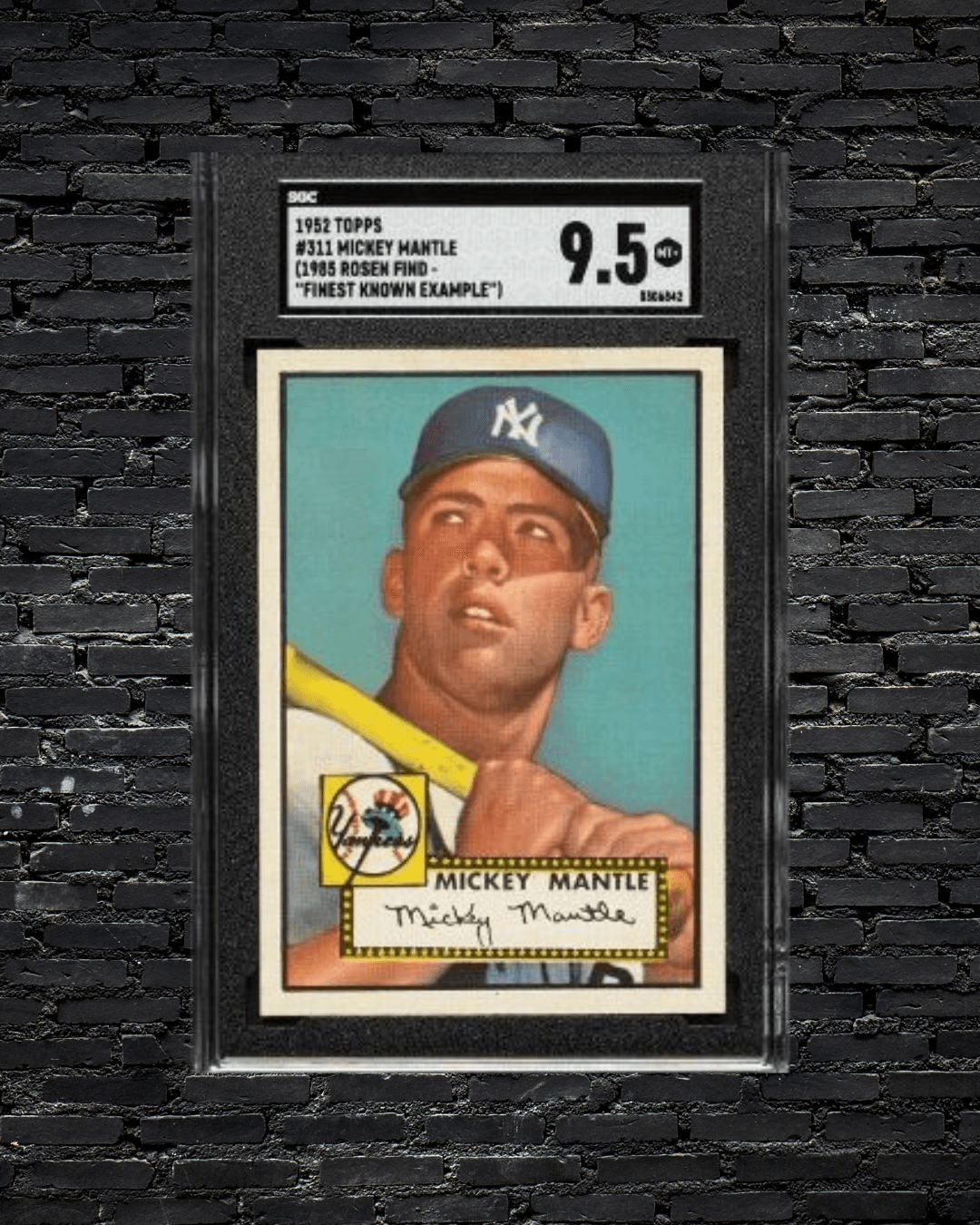

With $9 billion you stop being a retailer and start being the balance sheet of the category. The 1952 Mantle SGC 9.5 cleared $12.6 million. T206 Wagners trade $2-7 million depending on grade. First edition Charizard PSA 10 is $400-500K. Action Comics #1 CGC 9.0 just cleared $15 million in a private sale.

Own the comp in every vertical. You set the floor on every secondary market in the category. That's not retail. That's category-defining capital allocation.

7. Push inventory autonomy down to the store level.

Atlanta is sports cards. Brooklyn is comics. Seattle is MTG. Salt Lake City is vintage TCG. Norfolk is military memorabilia. The collector demographic is hyper-local. Every LCS owner in America already knows this.

Centralization killed every dying retail chain. The corporate buyer in a Texas office can't tell what sells in Brooklyn. The store manager in Brooklyn can.

GameStop should centralize the platform. Vault. Grading. Breaks software. Payments. League play. Marketing tools. Insurance. Then push 70-80% of inventory selection down to the operator on local signal. That's exactly what good local card shops do, which is why they outperform GameStop on engagement-per-customer in every market they share.

Tom Brady Beat Cohen With 14 Stores

This part is the box score.

Tom Brady's CardVault is at 14 locations. They're opening more than one new store per month. Targeting 25 by end of 2026. Authorized PSA, Beckett, and SGC submission on-site. Authorized retailers for Topps, Panini, Upper Deck, Pokemon, One Piece, Magic, Yu-Gi-Oh, and Fanatics Authentic. They run their own breaks through Fanatics Live.

Cohen had a six-year head start. He had $9 billion in cash. He had brand recognition with the exact buyer demographic. He had 1,600 stores already leased, staffed, and merchandised.

He got beaten on the play by a retired quarterback running 14 mall stores.

There's no spin on it. There's no "we have a different strategy" press release that fixes the ratio. The collectibles operator with 1/100th the store count and 1/1000th the cash built a more legitimate trading card retail business than the company that has been telling Wall Street it's pivoting to collectibles for two years.

And the Real Kicker. No Pokemon Collab.

This is the line on the cap table that the analyst class hasn't fully priced in.

The Pokemon Company International celebrated its 30th anniversary in 2026. Biggest single marketing event of the year for the entire collectibles category. Generational nostalgia play. Massive retail tie-in.

The chosen U.S. mass retail partner. Target. The "only U.S.-based mass retailer" partnered with TPC for the anniversary. 100+ exclusive items. Two-phase drop on May 2 and June 6. Apparel. Accessories. Beauty. Home goods. Food. Joe Jonas in the campaign. Pokemon GO timed research integrated in Target stores. Character meet-and-greets at the SoHo flagship. Mead Trapper Keeper revival. Caboodles. Lip Smacker. Starter jackets. Iconic 90s nostalgia partners stacked across every category.

eBay got a "curated 30th anniversary selection" too. Co-branded marketing. Promotional placement.

GameStop got nothing. Not a co-branded SKU. Not a single line item. Not a window cling. Nothing.

Read that one more time. The company that made collectibles 33% of revenue. The company that partnered with PSA for in-store grading drop-off. The company that built Power Packs around Pokemon. The company that has taken more than a million PSA submissions through its stores. The company that tells Wall Street every quarter it's a "collectibles destination."

Did not get the call.

Target got the call. eBay got the call. GameStop did not.

That tells you exactly how the IP holder views GameStop. Not as a strategic brand partner. As a downstream reseller. A box that sells the product after the marketing happens elsewhere.

GameStop is running a forecourt for someone else's gas station. And that's the one piece of the business that's actually growing.

The Cohen Pattern

Cohen has been sitting on $9 billion for four years building a Treasury bond ETF in a costume. The eBay bid is the move you make when you've run out of operational moves. Cut sales and marketing in half. Lever up. Run the synergies. Harvest the brand.

PE retail roll-ups have a track record. The track record is a graveyard.

Pokemon at MSRP is the only line on the income statement that's working, and TPC just told the market what they think of GameStop by partnering with Target instead. The hostile bid replaces the investor call Cohen hasn't held in 18 months.

The collectibles category doesn't need GameStop to win. It needs operators who actually understand the category to build the next chapter. CardVault is doing it with 14 stores. Whatnot is doing it live. Local card shops are doing it on Tuesday nights in Cleveland.

GameStop had every advantage. The cash, the footprint, the brand recognition, the demographic. They spent four years buying Treasury bills and ATM-offering their way to a war chest they can't deploy intelligently.

The eBay bid is the proof.